How I Almost Lost My Savings Buying Pet Supplies — And What I Learned About Protecting My Assets

I never thought a simple trip to buy dog food could threaten my financial stability. But after overspending on premium pet products and impulse purchases, I found myself draining my emergency fund. It wasn’t just about the money — it was about how easily everyday spending habits can undermine long-term asset preservation. This is my real story of falling into common financial traps in the pet care world and how I finally took control. What began as small, well-intentioned choices — organic treats, monthly flea preventatives, fancy collars — quietly escalated into a significant monthly expense that I hadn’t budgeted for. By the time I realized the damage, my savings were thinner, my stress levels higher, and my sense of financial security shaken. This experience became a wake-up call: loving your pet doesn’t have to mean sacrificing your financial health.

The Hidden Cost of Loving Your Pet Too Much

Pet ownership often feels like parenting, and that emotional bond is powerful. It’s natural to want the best for your furry companion — the safest food, the softest bed, the most effective flea treatment. But this desire, while well-meaning, can easily translate into overspending. I began justifying purchases by telling myself I was being a responsible pet owner. Organic dog treats? Necessary. A waterproof winter coat for my small terrier? Essential. Monthly subscription for dental chews? Preventative care. Each item seemed reasonable in isolation, but together, they formed a pattern of emotional spending masked as responsibility. The truth is, the pet industry is expertly designed to appeal to this emotional connection. Marketing emphasizes safety, health, and happiness, making it difficult to say no without feeling like you’re compromising your pet’s well-being.

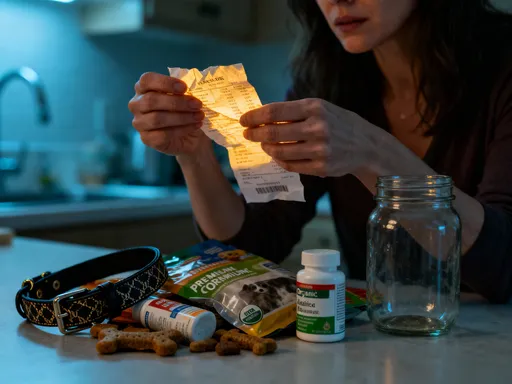

What I didn’t realize at the time was how quickly these small expenses accumulate. A $15 bag of treats every two weeks becomes $390 a year. A $40 grooming kit every month adds up to $480 annually. Designer leashes, specialty shampoos, calming sprays — none of these were emergencies, yet they became routine. When I finally reviewed my bank statements, I was stunned to see that my pet-related spending had overtaken my utility bills and was approaching the cost of my car insurance. That moment was a turning point. I began to see that unchecked emotional spending, even when driven by love, can quietly erode financial stability. The danger isn’t in buying one expensive item — it’s in the repetition, the normalization of premium spending without conscious evaluation.

This isn’t about guilt or shaming pet owners. It’s about awareness. The pet care market thrives on the assumption that higher price equals better quality, and that spending more is synonymous with caring more. But this equation isn’t always true. Many affordable products meet the same safety and nutritional standards as their premium counterparts. The emotional pull to spend, however, often overrides rational assessment. Recognizing this dynamic was the first step toward regaining control. I started asking myself not just whether a product was good for my pet, but whether it was necessary, whether a less expensive alternative existed, and whether the purchase aligned with my broader financial goals. This shift in mindset didn’t reduce my love for my pet — it deepened my sense of responsibility.

Why Pet Inflation Is Quietly Draining Your Wallet

Over the past decade, the cost of pet ownership has risen at a rate that many owners haven’t fully acknowledged. It’s not just inflation in general — it’s a specific trend in the pet industry where prices for food, medication, and preventive care have increased steadily. I used to buy a 20-pound bag of my dog’s favorite food for $45. Today, the same brand and size costs $65 — a 44% increase in just five years. At first, I assumed this was a temporary spike, a result of supply chain disruptions or ingredient shortages. But the prices never came back down. What felt like a short-term adjustment became the new baseline.

This trend isn’t isolated. Prescription medications, joint supplements, heartworm preventatives — all have seen significant price hikes. Even routine vet visits cost more than they did a few years ago, not because vets are overcharging, but because their own operational costs have increased. Equipment, staff wages, and pharmaceutical supplies all contribute to higher fees. I used to budget $500 a year for vet care. Now, that same level of care easily exceeds $900. The problem is that many pet owners don’t adjust their budgets accordingly. They continue planning as if pet costs are static, only to be blindsided when expenses rise. This lack of foresight can strain emergency funds, delay other financial goals, or lead to difficult choices when a medical crisis arises.

Another factor driving up costs is the dominance of premium brands. Supermarket shelves and online marketplaces are flooded with high-margin products that emphasize natural ingredients, grain-free formulas, or veterinarian recommendations. While some of these claims have merit, many are marketing tactics designed to justify higher prices. The result is that affordable, nutritionally sound options are harder to find — or harder to trust. I found myself defaulting to premium brands simply because they seemed more trustworthy, even when my vet assured me that store-brand alternatives were perfectly adequate. This perception gap — between actual value and perceived necessity — is where much of the financial drain occurs.

The reality is that pet ownership today requires a more robust financial plan than in the past. Ignoring inflation in this category is like ignoring rising housing or healthcare costs — eventually, it catches up with you. The solution isn’t to avoid quality care, but to acknowledge that pet expenses are no longer incidental. They are a core part of household spending, deserving of the same planning and budgeting as groceries, utilities, or transportation. By treating pet costs as a predictable, growing expense, rather than a series of surprises, you can protect your assets from erosion.

The Investment Mindset: Treating Pet Spending Like a Long-Term Commitment

One of the biggest financial mistakes I made was viewing my pet as a one-time expense rather than a long-term financial commitment. When I adopted my cat, I budgeted for the adoption fee, initial vaccinations, and a few supplies. I didn’t plan for the next 12 years. That changed when she developed a urinary blockage at age seven — an emergency that required hospitalization, surgery, and follow-up care. The total bill was nearly $3,000, a sum I hadn’t saved for. I had to dip into my emergency fund, which was meant for car repairs or job loss, not pet surgery. That experience forced me to rethink my entire approach.

Pets typically live 10 to 15 years, sometimes longer. Over that time, they will need routine care, vaccinations, dental cleanings, and likely some form of medical intervention. Chronic conditions like arthritis, diabetes, or kidney disease are common in older pets and can require ongoing treatment. These aren’t outliers — they’re expected parts of pet ownership. Yet most people don’t plan for them financially. This is where the investment mindset becomes essential. Just as you save for retirement, home repairs, or your children’s education, you should treat pet care as a long-term liability that requires proactive funding.

One effective strategy I adopted was setting up a dedicated pet savings account. Every month, I transfer a fixed amount — currently $75 — into this account. It’s not always easy, but automation makes it consistent. Over time, this fund has grown to cover routine expenses like flea prevention, grooming, and annual checkups, as well as larger unexpected costs. When my dog needed a minor ligament repair last year, the fund covered the $1,200 bill without touching my emergency savings. This approach turns unpredictable costs into planned expenditures, reducing financial stress and protecting your broader financial health.

Another tool I now use is a veterinary savings plan, similar to a health savings account. Some clinics offer payment plans or wellness packages that bundle preventive care at a discount. These can be cost-effective if you use the services, but they require careful evaluation. I compare the total annual cost of a plan to what I’d spend out of pocket to ensure it’s truly a savings. The key is intentionality — making deliberate choices rather than reacting to emergencies. When you treat pet care as a long-term financial commitment, you’re not just protecting your wallet; you’re ensuring that your pet receives consistent, high-quality care throughout their life.

Smart Substitutions That Save Without Sacrificing Care

One of the most empowering realizations I had was that not every premium product is worth the price. I began experimenting with alternatives, testing generics, store brands, and DIY solutions to see what worked. Some attempts failed — a cheap flea collar irritated my dog’s skin, and a bulk bag of kibble went stale before we finished it. But many substitutions performed just as well as their high-end counterparts, often at half the cost. This wasn’t about cutting corners; it was about spending smarter.

For example, I switched from a name-brand flea and tick treatment to a generic version recommended by my vet. The active ingredients were identical, and the price was 60% lower. I also began buying heartworm prevention in six-month supplies online, which reduced the per-dose cost by 30%. These aren’t risks to my pet’s health — they’re informed choices based on ingredient transparency and veterinary guidance. Similarly, I tried a store-brand dog food formulated for sensitive stomachs. After a two-week transition, my dog adapted well, and his coat and energy levels remained strong. I saved over $200 a year without compromising nutrition.

Grooming was another area where I found savings. Instead of monthly professional grooming, I now handle basic brushing, ear cleaning, and nail trimming at home. I invested in a quality brush and a nail grinder, which paid for themselves in three visits. For baths, I use a gentle, vet-approved shampoo in bulk. I still take my dog for a full groom twice a year — mainly for coat trimming — but reducing the frequency cut my grooming costs in half. I also discovered telehealth vet consults for minor issues like itchy skin or mild digestive upset. A 15-minute video call costs $40, compared to $80 for an in-person visit, and often results in the same advice: change the diet, try an over-the-counter remedy, or monitor symptoms.

The key to successful substitution is research and caution. I always consult my vet before switching medications or food, and I introduce changes gradually. I also read ingredient labels and avoid products with fillers or artificial additives, regardless of price. This approach allows me to maintain high standards of care while reducing monthly outflow. It’s not about deprivation — it’s about efficiency. By focusing on what truly matters for my pet’s health, I’ve eliminated unnecessary expenses and redirected those funds toward long-term savings.

Insurance or Self-Insuring? Weighing the Real Protection Options

When I faced that $3,000 surgery bill, I immediately looked into pet insurance. It seemed like the perfect solution — pay a monthly premium and have major costs covered. But after reviewing policies, I discovered significant limitations. Many plans have high deductibles, annual caps, and exclusions for pre-existing conditions. Some require you to pay upfront and wait weeks for reimbursement. I also found that premiums increase as pets age, sometimes doubling over a few years. In some cases, the total premiums paid over time exceed the cost of likely vet bills, especially for healthy pets. Insurance offers peace of mind, but it’s not a guaranteed financial win.

This led me to consider self-insuring — setting aside money each month to cover potential emergencies. I calculated the average annual cost of vet care for my dog’s breed and age, added a buffer for emergencies, and began saving accordingly. I now treat this like a non-negotiable expense, just like car insurance or retirement contributions. If a major issue arises, I have the funds ready. If not, the money continues to grow, serving as a financial cushion. Self-insuring gives me full control over how and when I spend, without claim denials or coverage limits.

The choice between insurance and self-insuring depends on your financial situation and risk tolerance. If you have limited savings and fear being unable to cover a $2,000 bill, insurance may be worth the cost. But if you can consistently save and prefer control over your funds, self-insuring may be more cost-effective in the long run. I ultimately chose self-insuring because it aligns with my goal of building wealth, not just transferring risk. That said, I acknowledge that insurance can be valuable for owners of breeds prone to expensive health issues or those who want psychological comfort. The important thing is to evaluate both options objectively, not out of fear or marketing pressure.

Whichever path you choose, the goal is the same: to protect your assets while ensuring your pet receives necessary care. The real protection isn’t in a policy document — it’s in having a plan. Whether through insurance, savings, or a combination of both, proactive financial preparation turns potential crises into manageable events. This is the essence of asset preservation: anticipating risks and building systems to absorb them without disruption.

Automating for Discipline: Building Financial Guardrails

Before I implemented systems, my pet spending was reactive and emotional. I bought what I saw in the store, responded to online ads, and made impulse decisions at the vet’s office. There was no structure, no limits. The turning point came when I introduced automation and boundaries. I set up a monthly transfer of $75 to my pet savings account, linked to my paycheck. This ensured consistent funding without relying on willpower. I also created a spending cap for discretionary pet purchases — $50 per month for treats, toys, or accessories. Once that limit is reached, I wait until the next month.

Another rule I adopted was the 48-hour delay for non-essential purchases. If I see something I want — a new toy, a specialty supplement — I wait two days before buying. In most cases, the urge passes, or I realize it’s not necessary. This simple behavioral nudge reduced my impulse spending by more than half. I also unsubscribed from marketing emails and limited my time on pet supply websites. These digital guardrails minimized temptation and kept my focus on long-term goals.

Integration was key. I didn’t treat pet expenses as a separate category but included them in my overall financial plan. I reviewed them during monthly budget check-ins, just like groceries or entertainment. This holistic view helped me see how pet spending affected my ability to save for vacations, home repairs, or retirement. When I noticed it was crowding out other priorities, I adjusted. Automation and rules didn’t eliminate spending — they made it intentional. I still buy my dog new toys and special treats, but now it’s within a framework that protects my financial health.

Behavioral finance teaches us that discipline is easier with systems than with self-control alone. By designing my environment to support good decisions, I reduced the mental load and emotional strain of managing pet costs. The result has been greater peace of mind, stronger savings, and a more sustainable approach to pet ownership. Financial guardrails don’t restrict freedom — they create the stability that makes lasting care possible.

Turning Awareness Into Lasting Financial Health

The journey from financial stress to stability didn’t happen overnight. It began with a single moment of awareness — looking at my bank statement and realizing I was spending more on my dog than on my own healthcare. That discomfort sparked change. I stopped viewing pet spending as an unavoidable expense and started seeing it as a series of choices. Each purchase became an opportunity to align my actions with my values: loving my pet deeply, but not at the cost of my financial security.

True financial wellness isn’t about deprivation. It’s about intentionality. It’s understanding that protecting your assets isn’t selfish — it’s responsible. When you have a solid financial foundation, you’re better equipped to handle emergencies, provide consistent care, and avoid the stress of unexpected bills. In this way, financial discipline enhances, rather than diminishes, your ability to care for your pet. A well-funded pet savings account is a form of love — it ensures that when your companion needs you most, you’ll be able to respond without fear or compromise.

The lessons I’ve learned extend beyond pet ownership. They apply to any area where emotion influences spending — parenting, home maintenance, even holiday gifts. The principles remain the same: recognize emotional triggers, plan for long-term costs, seek value without sacrificing quality, and build systems that support consistency. By applying these strategies, I’ve not only protected my savings but also gained confidence in my financial decisions.

Loving your pet doesn’t require financial sacrifice. It requires strategy. With awareness, planning, and small, consistent actions, you can provide excellent care while preserving your wealth. That balance — between compassion and prudence — is the hallmark of lasting financial health. And in the end, that’s the greatest gift you can give both yourself and your beloved companion.